The investment landscape for federal employees has delivered a powerful burst of growth, offering a prime opportunity to review asset allocations. According to the latest monthly performance reporting from the Federal Retirement Thrift Investment Board (FRTIB), every single underlying portfolio within the Thrift Savings Plan (TSP) finished in the black for the second consecutive month.

Led by aggressive gains in equities, the three core stock funds achieved significant milestones. While these surging balances provide a welcome boost to federal retirement accounts, capitalizing on market momentum requires look past short-term gains to execute a disciplined, risk-managed allocation strategy.

Inside the Numbers: High-Performing Equities Take Center Stage

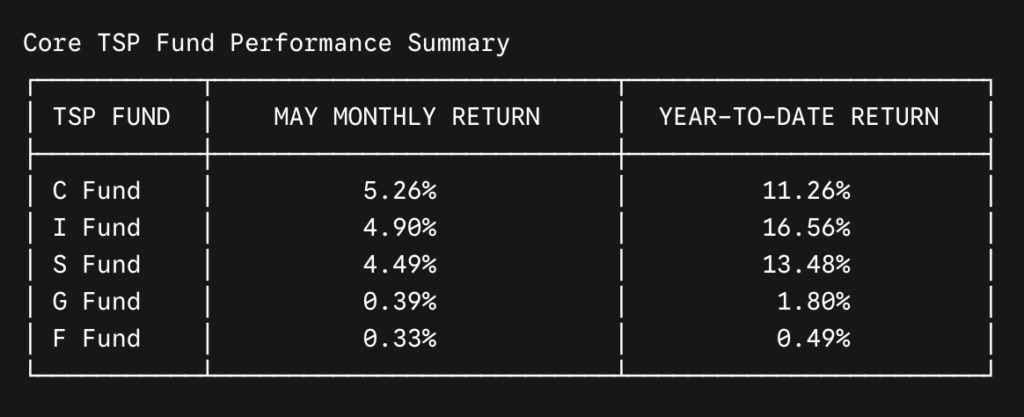

The performance metrics show that equity-based core funds captured the lion’s share of the market’s upward trajectory. The C Fund (Common Stock Index Investment Fund), which tracks the S&P 500, anchored the month’s performance by climbing 5.26 percent over the 31-day period. This surge elevates the C Fund’s year-to-date (YTD) performance to 11.26 percent, sustaining its position as a primary vehicle for domestic equity growth.

The international equities of the I Fund captured second place for monthly growth, gaining 4.90 percent. Thanks to strong international market performance earlier in the year, the I Fund leads all core funds on a year-to-date basis with an impressive 16.56 percent net expansion. Meanwhile, the S Fund (Small Capitalization Stock Index Fund) completed the equity sweep by gaining 4.49 percent, driving its YTD returns up to 13.48 percent.

In contrast, conservative fixed-income portfolios generated minor, steady steps forward. The G Fund (Government Securities Investment Fund) advanced by its statutorily mandated rate of 0.39 percent, bringing its YTD progress to 1.80 percent. The F Fund (Fixed Income Index Fund) also notched a minor gain of 0.33 percent, positioning its YTD return at 0.49 percent.

Understanding the Lifecycle Glide Path Response

The universal upswing across core funds naturally carried over to the TSP’s diversified Lifecycle (L) Funds. Designed as “set-and-forget” target-date mini-portfolios, L Funds automatically recalibrate every three months, shifting toward a more conservative allocation as a participant’s targeted retirement date approaches.

Reflecting their high concentration of equity holdings, target portfolios geared toward late-career and early-career professionals—including the L 2055, L 2060, L 2065, L 2070, and L 2075 Funds—all posted a strong, uniform 5.00 percent gain.

Conversely, portfolios tailored for immediate or near-term withdrawals moved at a more measured pace:

- L Income Fund: Gained 1.66% (YTD: 4.93%)

- L 2030 Fund: Gained 2.95% (YTD: 8.10%)

- L 2040 Fund: Gained 3.71% (YTD: 10.03%)

While the passive, automatic rebalancing of L Funds offers excellent defense against emotional over-trading during market swings, it can occasionally create a strategic blind spot. For instance, if an individual plans to continue working past their projected target year, their TSP assets will continue sliding down the “glide path” directly into the conservative L Income Fund. This transition can inadvertently cap growth potential right when an employee needs to outpace inflation.

The Rebalancing Dilemma: Managing Wealth in an Inflationary Environment

Strong stock market gains create an underlying challenge for retirement planning: asset drift. When equities rapidly outperform fixed income, an employee’s total portfolio can quickly become over-exposed to stock market volatility. A portfolio originally structured as a balanced 60/40 split can easily drift into an aggressive 75/25 distribution after consecutive months of stock market growth.

If the market experiences a sudden correction, an unmanaged, top-heavy portfolio faces enhanced drawdown risks. Conversely, moving entirely into the G Fund to lock in profits introduces a different threat—inflationary erosion. With consumer price indexes indicating consistent upward pressure on everyday goods, maintaining a retirement portfolio that fails to outpace inflation can silently diminish long-term purchasing power.

Proactive Investment Management Strategies for Federal Personnel

To capture market upside while protecting your accumulated nest egg, federal professionals should move beyond passive monitoring and adopt a disciplined portfolio framework:

- Execute an Asset Allocation Audit: Log into your TSP account and review your current fund distribution. Compare your actual allocation against your target risk profile to identify and correct any unintended asset drift.

- Synchronize Contribution Milestones: Take full advantage of the updated contribution thresholds. For instance, the regular elective deferral limit allows employees to shield up to $24,500 pre-tax. For workers utilizing catch-up contributions, ensure your allocations automatically spill over correctly without exceeding statutory boundaries.

- Analyze the Roth Conversion Window: Strong fund growth provides an excellent baseline for evaluating the newly deployed TSP Roth In-Plan Conversion option. Converting a portion of your traditional earnings into a tax-free Roth account during periods of market strength can permanently insulate your investment growth from future tax hikes.

Integrating Market Growth with Comprehensive Financial Planning

A growing TSP balance is an exceptional asset, but it is only one piece of a complete federal retirement puzzle. Building a secure retirement requires looking past basic investment returns to evaluate how your TSP wealth coordinates with your Federal Employees Retirement System (FERS) annuity, Social Security projections, Federal Employees Health Benefits (FEHB) continuity, and lifetime tax exposures.

This is where specialized, external guidance becomes indispensable. Internal Benefit Advisors provides comprehensive financial education, tax strategy optimization, life insurance restructuring, and holistic retirement planning designed specifically for federal, postal, and state employees.

Whether you need to fine-tune your asset allocations to protect recent stock market gains, navigate the complex rules of a Roth in-plan conversion, or construct a resilient retirement transition plan that ensures your wealth remains secure throughout your post-service years, working with a specialized advisor ensures your future remains stable, maximized, and entirely under your control.

References

- Federal Retirement Thrift Investment Board (FRTIB). (2026). Thrift Savings Plan Monthly Performance Report: May 2026 Operations Insight. Codified at 5 CFR Part 1601.

- FedWeek. (2026). TSP Stock Funds Post Strong Gains in May; Up 11-16 Percent on Year. https://www.fedweek.com/fedweek/tsp-stock-funds-post-strong-gains-in-may-up-11-16-percent-on-year/

- Government Executive. (2026). TSP Funds Kept Climbing in May. https://www.govexec.com/pay-benefits/2026/06/tsp-funds-kept-climing-may/413881/

- Thrift Savings Plan Official Portal. (2026). Rates of Return and Fund Share Price History. https://www.tsp.gov/fund-performance/

- Internal Benefit Advisors LLC. Retirement Planning Support and Benefits Package Education for State and Federal Employees. https://internalbenefitadvisors.com