Federal employees facing a career-altering medical condition often encounter a confusing bureaucratic crossroad: choosing between the Federal Employees’ Compensation Act (FECA) and FERS Disability Retirement. As highlighted by FEDweek, understanding the structural and financial differences between the Department of Labor’s (DOL) workers’ compensation program and the Office of Personnel Management’s (OPM) retirement benefit is critical to securing your long-term livelihood.

A medical crisis is stressful enough without the added burden of navigating competing federal agencies. Making the wrong election can result in thousands of dollars in lost income or a sudden, devastating lapse in your health insurance.

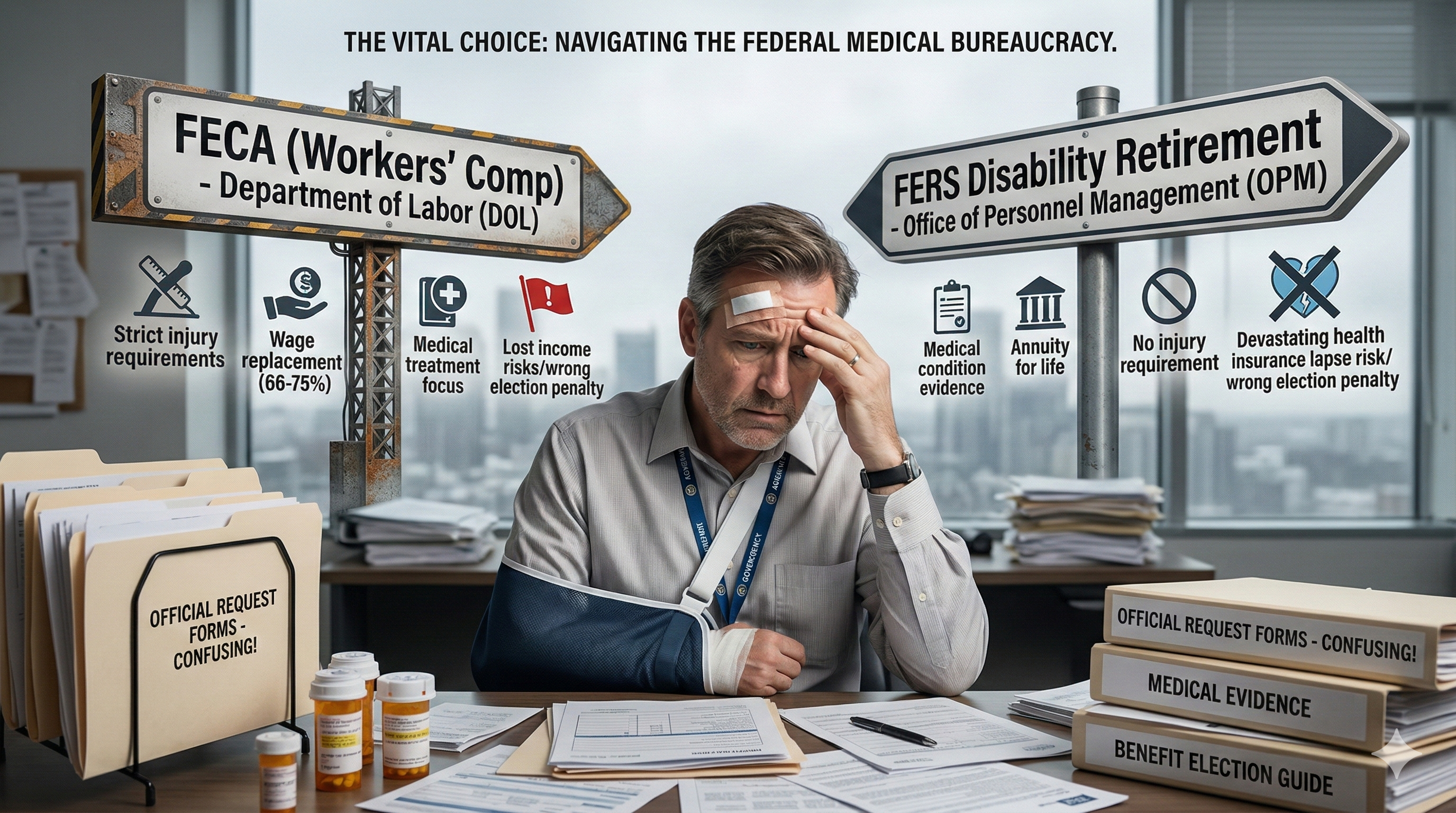

🏛️ The Core Difference: Causation and Jurisdiction

The most fundamental difference between the two programs lies in how you were injured and who controls the checkbook.

1. FECA (Workers’ Compensation)

- The Requirement: To qualify for FECA, your injury or illness must be strictly job-related (sustained in the performance of duty) or an occupational disease caused by your federal employment.

- The Agency: Claims are adjudicated and managed by the DOL’s Office of Workers’ Compensation Programs (OWCP).

- The Goal: FECA is designed as a temporary wage-replacement and rehabilitation program to eventually return you to the workforce. It is not a retirement system.

2. FERS Disability Retirement

- The Requirement: To qualify for FERS Disability, your medical condition does not need to be work-related. Whether you suffered a weekend sports injury, a car accident, or developed a progressive illness, you only need to prove that the condition prevents you from performing the essential functions of your specific position for at least one year. You must also have at least 18 months of creditable civilian service.

- The Agency: Claims are adjudicated by OPM.

- The Goal: This is a permanent retirement benefit that transitions you out of the federal workforce entirely.

📉 Sound Data: The Massive Financial Gap

When it comes to your monthly cash flow, the two programs operate in completely different financial universes.

- The FECA Advantage: FECA benefits are highly lucrative. If you have an approved claim and at least one dependent, FECA pays 75% of your regular salary. If you have no dependents, it pays 66.6%. Most importantly, FECA wage-loss compensation is 100% tax-free.

- The FERS Reality: FERS Disability Retirement pays significantly less. For the first 12 months, OPM pays 60% of your High-3 average salary. After the first year, the payment drops drastically to 40% of your High-3. Unlike FECA, FERS Disability payments are fully taxable at the federal (and often state) level.

- The Net Difference: For an employee earning $100,000 a year with dependents, FECA provides $75,000 of tax-free income. The exact same employee on year two of FERS Disability Retirement would receive $40,000 of taxable income—a staggering $35,000+ reduction in net purchasing power.

⚠️ The “Concurrent Receipt” Rule and Abeyance

Federal law prohibits “dual compensation.” You cannot simultaneously receive FECA wage-loss benefits and a FERS Disability Retirement annuity for the exact same period of time. You must elect one or the other.

Because FECA pays substantially more and is tax-free, nearly all eligible employees elect to receive OWCP benefits. However, relying solely on FECA is a massive risk. OWCP can force you to undergo “second opinion” medical exams, assign you to vocational rehabilitation, or abruptly terminate your benefits if a DOL doctor claims you have recovered.

The Golden Strategy: You should aggressively pursue approval for both programs. Once approved for both, you formally elect to receive the higher-paying FECA benefits while placing your FERS Disability Retirement in a frozen status known as “abeyance.” If the DOL ever cuts off your workers’ compensation, you simply notify OPM to “turn on” your FERS pension, ensuring you are never left without an income.

🛡️ Secure Your Medical Transition

Transitioning out of federal service on medical grounds requires precise timing and flawless paperwork. Missing the one-year filing deadline for FERS Disability Retirement after you separate can permanently destroy your safety net.

Internal Benefit Advisors specializes in the complex intersection of federal medical separations, OPM processing, and lifetime benefit preservation.

How We Help You Navigate a Medical Exit:

- The Abeyance Strategy: We help you structure your applications so that you successfully lock in FERS Disability Retirement approval while maximizing your tax-free FECA income, ensuring a seamless transition if DOL terminates your claim.

- FEHB Preservation: To carry your Federal Employees Health Benefits (FEHB) into retirement, you must meet specific continuous-coverage rules. We verify that your time on Leave Without Pay (LWOP) or FECA does not inadvertently disqualify you from lifetime health coverage.

- Social Security Coordination: Both FERS Disability and FECA interact heavily with Social Security Disability Insurance (SSDI). We calculate the mandatory OPM offsets so you aren’t hit with a massive overpayment bill from the government months after you retire.

Do not let a medical emergency destroy the financial security you have spent your career building.

Would you like me to outline the specific OPM filing deadlines for FERS Disability Retirement to ensure your safety net does not expire?

References

- FEDweek. “The Key Differences Between Disability Retirement and FECA Benefits.” Retirement & Financial Planning Report. 2026.

- U.S. Office of Personnel Management (OPM). FERS Information: Disability.

- U.S. Department of Labor (DOL). Office of Workers’ Compensation Programs (OWCP): FECA.

- Internal Benefit Advisors. Retrieved from https://internalbenefitadvisors.com